Abstract

Packaged TRM systems have dominated capital markets for decades. Yet modern open‑source pricing and risk frameworks—such as QuantLib, Open‑Source Risk Engine (ORE), RatesLib, Strata, and Finmath—are changing expectations. These libraries now provide industrial‑strength analytics, transparent risk modelling, and extensible simulation engines. As a result, TRM systems can be built faster and more flexibly. In parallel, AI development tools reduce coding time and simplify system assembly.

This paper compares packaged TRM systems with AI‑driven custom platforms and highlights when each approach is the better choice.

1. Introduction

TRM systems traditionally require large budgets, long delivery cycles, and significant vendor involvement. Many implementations take 2–5 years and involve dozens to hundreds of FTEs. Some projects even fail after years of effort. Meanwhile, open‑source quant libraries have matured.

QuantLib offers a comprehensive pricing and risk framework widely used across the financial industry.

ORE extends QuantLib to deliver transparent pricing, XVA, exposure analytics, and simulation models designed as a foundation for tailored risk solutions.

Moreover, ORE continues to evolve. For example, the 2026 v15 release added enhanced Monte Carlo models, commodity curve interpolation, historical calibration tools, and expanded instrument coverage.

Similarly, RatesLib provides a modern Pythonic alternative with strong fixed‑income and FX functionality.

In addition, Strata and Finmath deliver Java‑based analytics frameworks used widely across quant development.

These tools create a strong foundation for building custom TRM systems with far less effort than before.

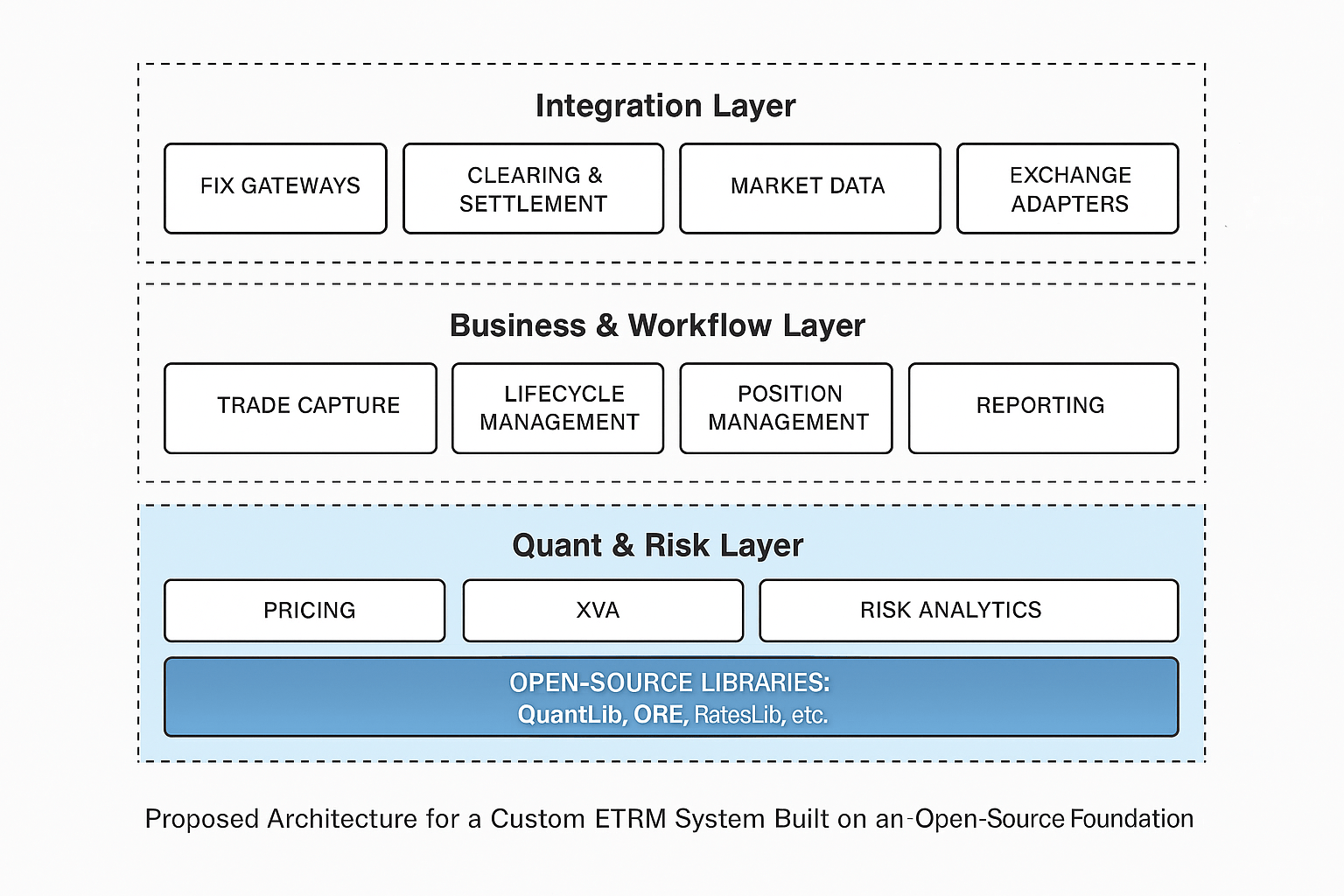

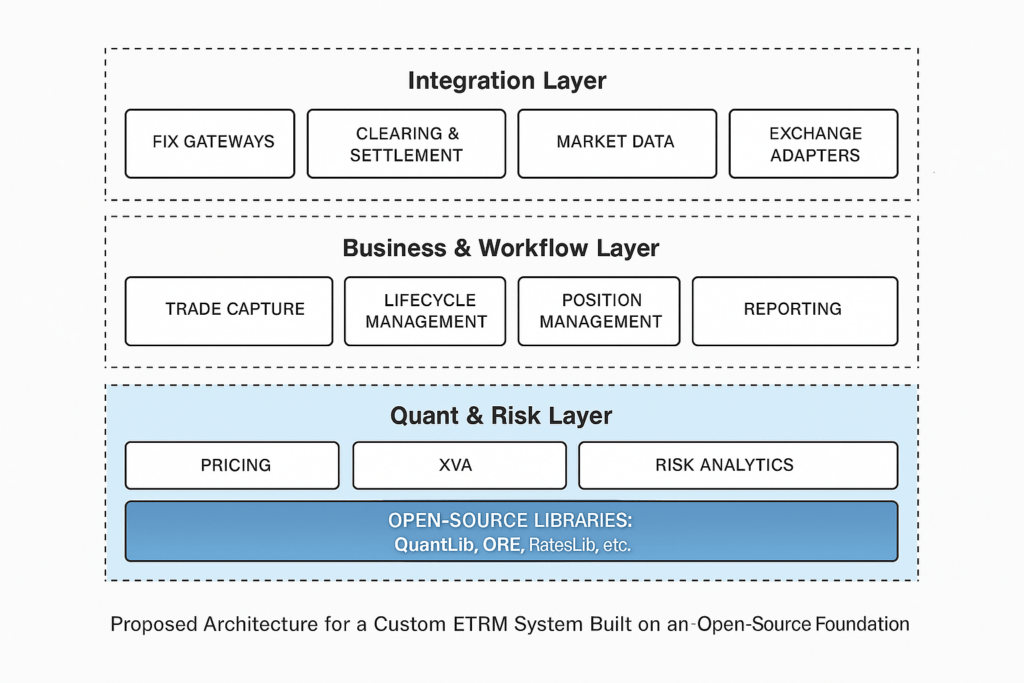

2. The Open‑Source TRM Foundation

2.1 QuantLib

QuantLib is a free, open‑source library for modeling, pricing, and risk management. It is widely used by practitioners, researchers, and commercial vendors. It offers valuation across asset classes and supports Python, C#, Java, and R. [quantlib.org]

2.2 Open‑Source Risk Engine (ORE)

ORE provides a complete risk and XVA framework. It extends QuantLib with simulation, exposure, valuation adjustments, stress testing, and configuration APIs. It was explicitly created as a transparent, peer‑reviewed foundation for custom risk systems.

Its faster development continues; ORE v15 added advanced models, flat‑forward commodity interpolation, extended AMC pricing, and improved calibration tools. [opensourcerisk.org] [lseg.com]

2.3 RatesLib

RatesLib offers a clean, modern Python design. It includes fixed‑income models, FX options, credit instruments, and multi‑currency analytics. It is easier to extend than C++‑based libraries. [superblocks.com]

2.4 Strata and Finmath

Strata provides sophisticated Java‑based analytics and scenario tools. Finmath offers Monte Carlo, XVA, and pricing engines for production use. Both are widely recognized in the quant ecosystem. [vlinkinfo.com]

Together, these projects offer a wide choice of mature, well‑tested quantitative foundations.

3. Packaged TRM Systems

Packaged TRMs like Murex, Calypso, etc, deliver broad instrument coverage, lifecycle automation, connectivity to clearing houses, and regulatory modules.

Advantages

- Integrated trade lifecycle

- Mature regulatory reporting

- Vendor-supported installation and documentation

Limitations

- Long implementation cycles

- High upgrade cost

- Black‑box pricing

- Banks often use only a fraction of available modules

- Vendor lock-in slows innovation

4. AI‑Driven Custom TRM Systems

AI development tools reduce coding effort and accelerate delivery. Combined with open‑source quant libraries, they enable modular, clean‑architecture TRM platforms.

Advantages

- Transparent risk and pricing (ORE is designed for transparency) [opensourcerisk.org]

- Modular architecture; build only required components

- Faster delivery cycles

- Lower TCO due to no license fees

- Full control over workflows and product definitions

- Easy integration with open protocols

Team Structure

A modern TRM can be built by:

- 1 Architect

- 6–12 Developers (AI‑augmented)

- 2 Business Analysts per module

- 1 DevOps

- 1 QA Automation Engineer

This is far smaller than traditional vendor‑based programs.

5. Comparison Summary

| Category | Packaged TRM | Custom AI‑Built TRM |

|---|---|---|

| Transparency | Low | High |

| Time to Market | Slow | Fast |

| TCO | High | Low |

| Customization | Limited | Full |

| Upgrade Burden | Heavy | Light |

| Instrument Breadth | Very broad | Library‑dependent |

| Risk Model Visibility | Opaque | Fully transparent (ORE/QuantLib) |

6. When Each Approach Wins

Choose Packaged TRM When:

- You need very broad exotic coverage

- Out‑of‑the‑box regulatory modules are essential

- You have limited internal engineering capability

Choose Custom TRM When:

- You need transparency in pricing and risk

- Want shorter delivery cycles

- Lower cost and faster change

- Your product universe is focused (FI, FX, commodities)

- Complete control of workflows

7. Conclusion

The TRM landscape is changing. Mature open‑source quantitative engines—QuantLib, ORE, RatesLib, Strata, and Finmath—provide strong pricing and risk foundations. Their transparency and extensibility, combined with modern AI development, allow banks to build modular, efficient, and highly customized TRM platforms.

Packaged TRMs remain valuable for broad coverage and regulatory completeness. However, for many institutions, a lightweight, AI‑assisted, open‑source‑based TRM is becoming not only viable but strategically superior.